Article

Implementing the Heston Stochastic Volatility Model for Equity Derivatives Pricing

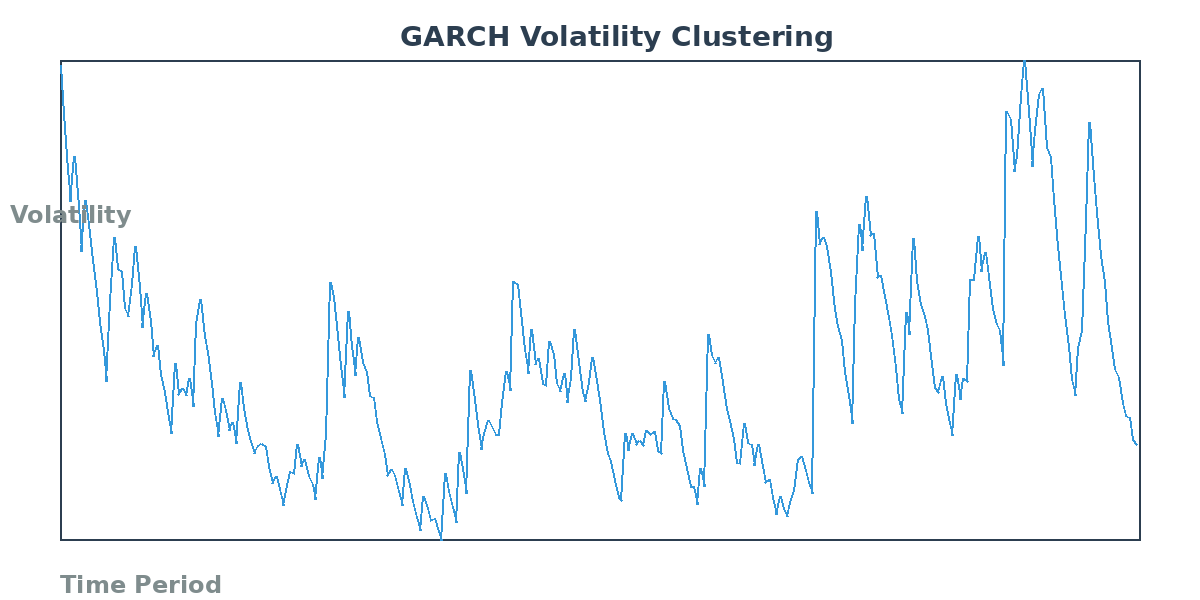

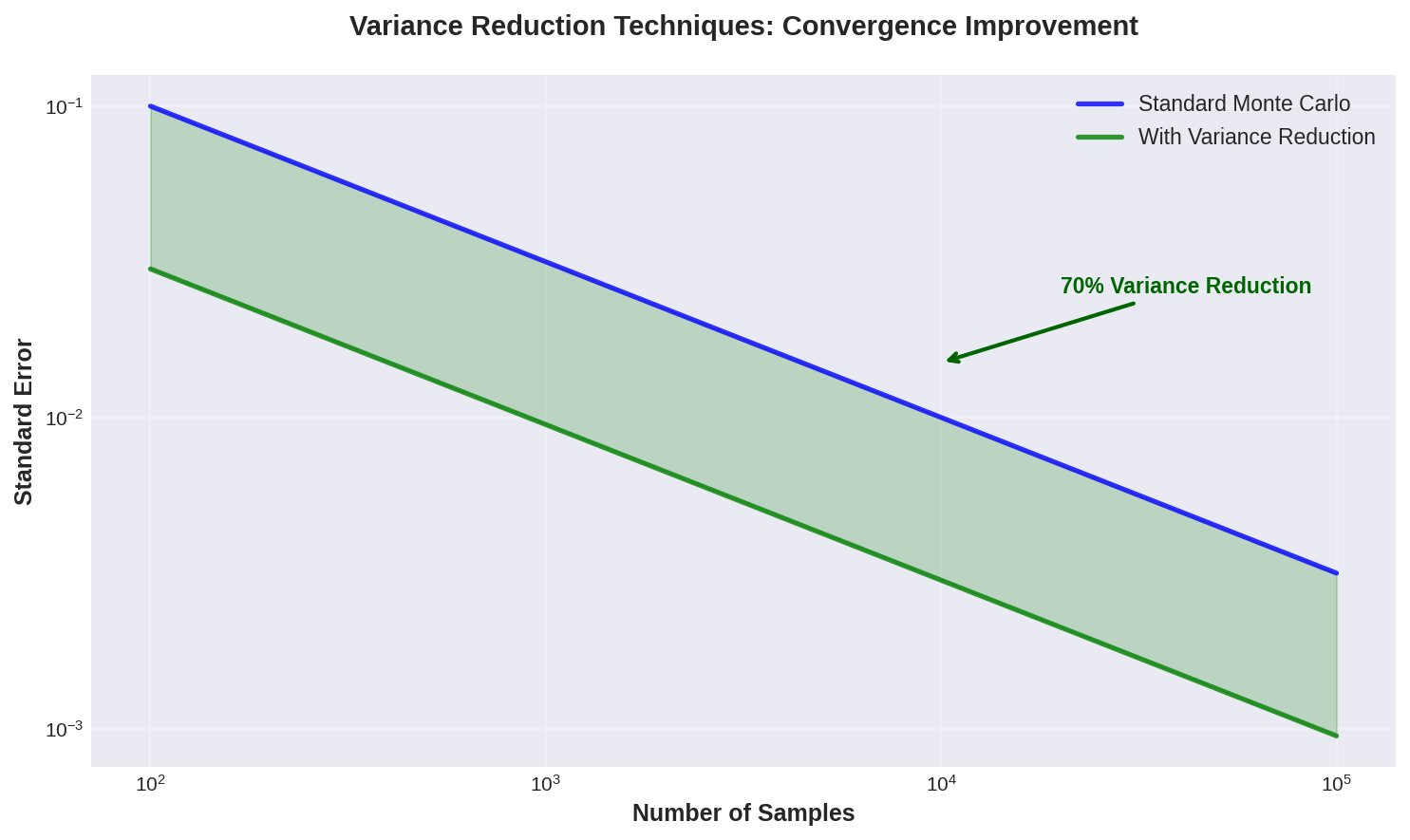

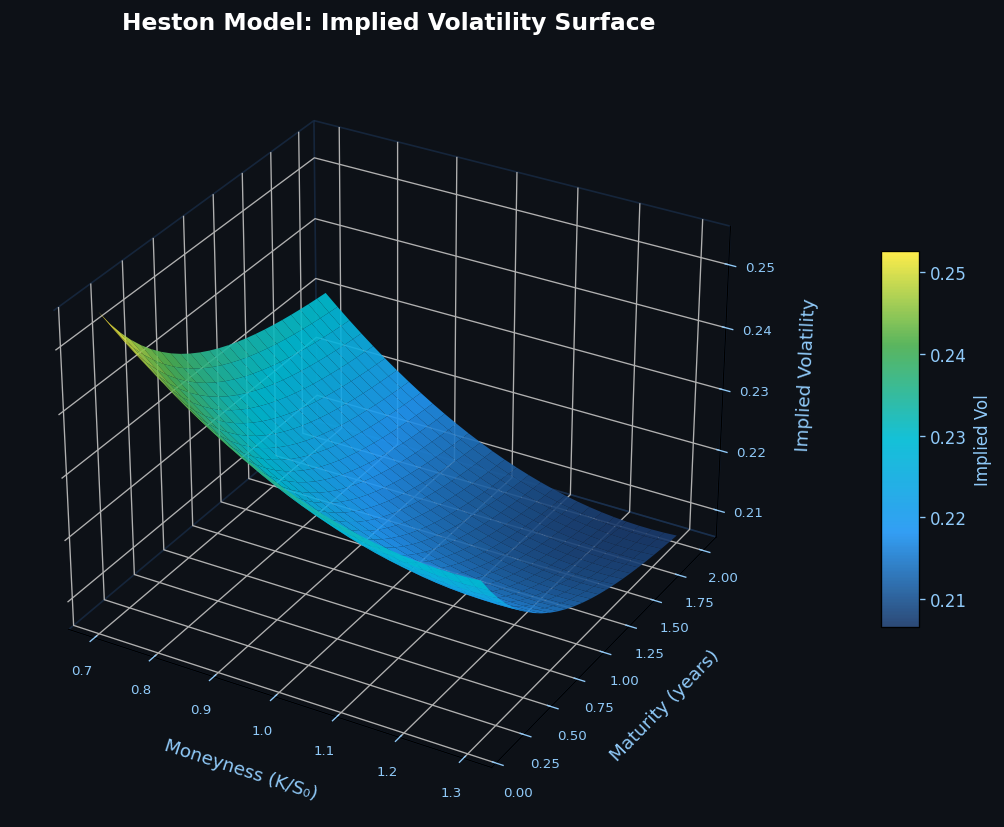

The Heston stochastic volatility model is the industry-standard framework for pricing equity derivatives with realistic volatility smiles. This article covers the model's mathematical structure, semi-analytical pricing via the characteristic function, calibration to market implied volatility surfaces, and Monte Carlo simulation using the full-truncation discretization scheme, with practical Python implementations throughout.

By Jeff

43 views